The 2024 Federal Budget, tabled on April 16, 2024, provides a mix of expected measures and a few surprises. In line with the announcements leading up to Budget Day, Budget 2024 outlines a multitude of measures targeted at housing affordability and the cost of living.

2024 Wellington-Altus Corporate Tax Reference Card Personal Tax Planning Cards LIF and RLIF Minimum & Maximum Factors Personal and Corporate Tax Integration Reference Cards 2024

Canadians have access to a plethora of tax-preferred vehicles for saving and investing, each of which provides unique planning opportunities and trade-offs, as well as their own rules and conditions that must be followed.

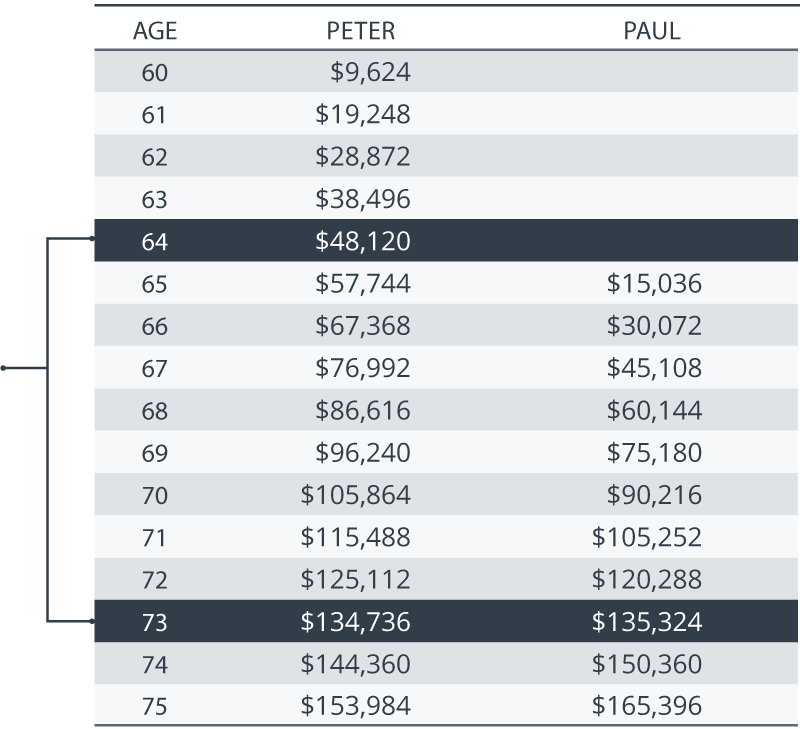

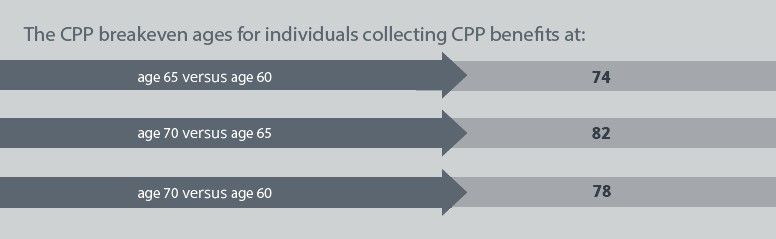

Most Canadians are familiar with CPP, which provides retirement, disability, survivor, and death benefits for individuals that have been employed in Canada.1 CPP is funded by mandatory annual contributions by employees, employers and self-employed individuals based on their CPP pensionable earnings, which typically include salary, wages or other remuneration, commissions, bonuses, most taxable benefits, and tips/ gratuities.